If you’re not sure what the difference is between a Financial Planner and an Investment Advisor, you’re not alone.

Let’s fix that.

What's the Difference Between a Financial Planner and an Investment Advisor?

Here’s the quick answer.

A Financial Planner helps you create the big-picture plan for your entire financial life, from your monthly budget, to planning your investment strategy, retirement, risk management, taxes, and your estate.

An Investment Advisor helps you carry out the “investment” part of your financial plan, like what stocks, bonds, and ETFs to buy or sell.

If you want to look closer at the differences, and see an example, keep reading.

Complete Breakdown: Financial Planner vs. Investment Advisor

Here’s an easy to understand breakdown that helps me explain Financial Planner vs. Investment Advisor to my clients.

What is a Financial Planner?

A Financial Planner is the person who helps you plan and manage everything that impacts your money. It’s about much more than just your investments.

1. Get the Complete Picture: When you start working with a Financial Planner, they’ll learn about your age, income, expenses, debt, investments, family size, and pretty much anything else in your life related to money.

2. Define Your Goals: Once they have a big picture view into your financial life, a Financial Planner will learn about your short-term and long-term goals.

3. Create Your Financial Plan: After they figure out where you are, and where you hope to be in the future, your Financial Planner will create a financial plan that accounts for everything in your life related to money.

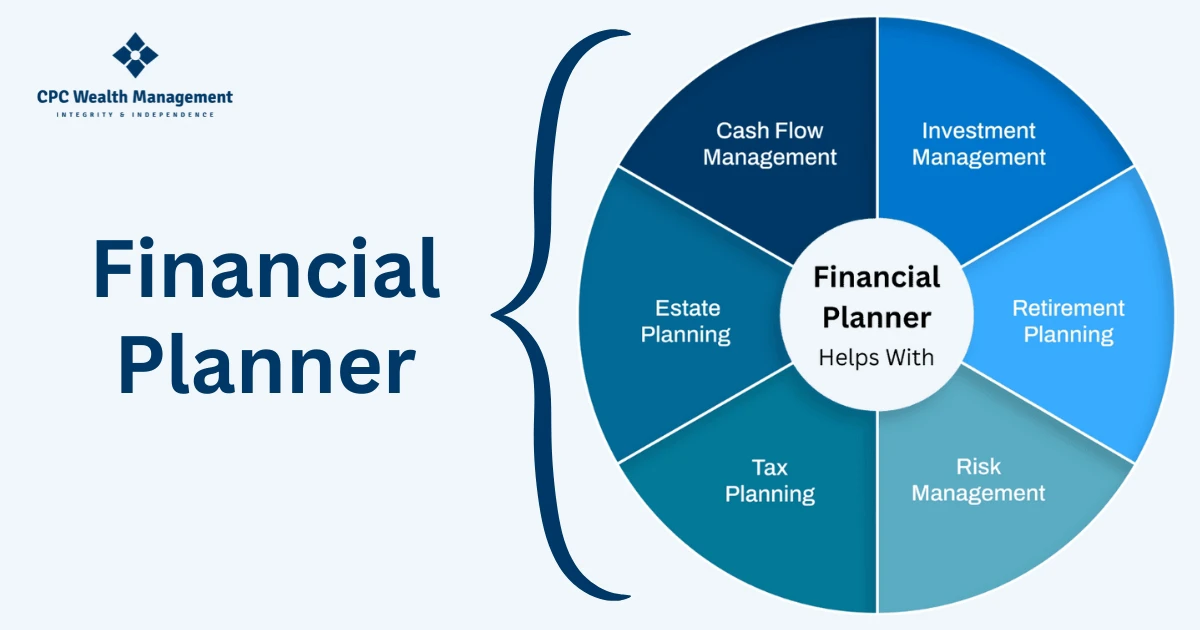

How does a Financial Planner help you?

Your financial plan covers these 6 key areas:

Cash Flow Management: Making a budget so that you understand your income and expenses. Then figuring out how much of your income to allocate towards retirement savings, investments, and other goals you may have.

Investment Management: Deciding how much money to allocate to your investments and creating your general investment strategy.

Retirement Planning: Saving for retirement and choosing the types of retirement accounts that will work best for you.

Risk Management: Managing your risk with products such as insurance policies and strategies like diversifying your investments.

Tax Planning: Understanding how the financial decisions you make impact your taxes, while using strategies to reduce your taxes now and in the future.

Estate Planning: Protecting your estate for your family with products like wills and trusts.

What a Financial Planner does not do

Unless your Financial Planner is also an Investment Advisor, they won’t be able to:

Make recommendations about specific stocks, bonds, ETFs, mutual funds and other securities.

Manage accounts where they buy and sell stocks, bonds, ETFs, mutual funds and other securities for you.

Do Financial Planners have to be licensed?

There’s no license required to call yourself a Financial Planner, and you’re not required to hold any specific certifications.

As the client, that makes it tough to figure out if the person calling themselves a “Financial Planner” is actually qualified. But there are certifications you can look for.

What is a Certified Financial Planner (CFP®)?

If someone is a CFP® professional, it means that they’ve had extensive training, passed a rigorous exam, and follow strict ethical standards.

When it comes to your finances, you deserve to have confidence in the person you work with. That’s especially true here in Westchester County, NY, where the median household income and cost of living are all significantly higher than national averages. With so much more at stake, the tiniest mistake can have huge implications.

That’s one of the reasons I became a CFP® professional before starting CPC Wealth Management, so that we can bring the highest level of expertise to every client relationship.

What is an Investment Advisor?

Part of your financial plan is figuring out how much money you can invest, the general types of investments you might want to consider, and how much risk you can take. But a Financial Planner can’t give you advice about which specific investments are right for you.

That’s why you need an Investment Advisor to help you execute the “Investment” part of your financial plan. Your Investment Advisor is the expert that can recommend specific investments.

What does an Investment Advisor help with?

Recommend Specific Investments: Advises you which stocks, bonds, ETFs, mutual funds and other investments to buy or sell.

Investment Account Management: Helps you open your brokerage accounts and place orders to buy and sell different investments.

Investment Risk Management: Helps manage your investment risk with diversification and other advanced strategies that can help to limit losses.

General Investment Strategy: Helps you to understand the market and the economy so that you can make adjustments to your overall investment strategy as needed.

What an Investment Advisor does not do:

Unless your Investment Advisor is also a Financial Planner, they won’t help with:

Retirement planning

Managing your budget

Managing overall financial risk with insurance products

Comprehensive tax planning

Planning your estate

Do Investment Advisors all have to be licensed?

Yes. Unlike Financial Planners, Investment Advisors are legally required to be licensed. All Investment Advisors have to hold a Series 65 License so they can:

Recommend stocks, bonds, ETFs, and other securities for you to buy or sell

Place buy and sell orders in your brokerage account (with your permission)

You can use FINRA’s BrokerCheck to see what licenses a person has.

A Real World Example

Financial jargon is always easier to understand when you have an actual example. Here’s one that might be helpful.

Earlier this year, a young couple from Scarsdale, NY came in. They weren’t sure if they needed financial planning, or if they should start with an Investment Advisor. I started by learning a bit about the couple.

About the couple:

Recently married,

Had no debt except for student loans,

The husband was a business owner, and the wife worked for a large company,

Had about $120,000 saved that they weren’t sure what to do with.

The couple's goals:

Buy a house within the year,

Have their first child within 5 years,

Invest for their future (if they had enough money),

Make sure they were making the right choices with their money.

First, they needed a Financial Planner

I recommended the couple start with a Financial Planner to help:

Assess their present income and expense levels.

Determine an appropriate emergency fund.

Utilize the most efficient retirement savings vehicle.

Confirm they are fully taking advantage of the benefits offered by the wife’s company.

Assess their protection requirements, including but not limited to renters, auto, and disability insurance, to verify sufficient coverage is maintained.

Establish a systematic savings plan for their down payment on their future house.

Educate them on risk tolerance and aligning that with their investment choices.

Then, they also needed an Investment Advisor

The couple needed most of their savings in the short-term to use for a down-payment on their house. But there was a little left over that they could invest.

Their monthly budget also allowed them to save 5% of their income to put towards investments each month.

So we knew they also needed an Investment Advisor to:

Give advice about which stocks, bonds, and other investments to buy

Manage their brokerage accounts for them

Your life is always easier when you can find a Financial Planner and an Investment Advisor at one financial firm.

Why Having Both Under One Roof Matters

Your Financial Planner is like the coach of your team. They see the big picture, write the playbook, and make sure everything in your financial life fits together.

Your Investment Advisor is the quarterback. They run the plays and make key decisions in real time to execute the coach’s strategy. But instead of scoring touchdowns, they’re focused on growing your investments.

Just like in football, the game plan works better when your coach and quarterback are in sync.

The reality is, the decisions your Investment Advisor makes overlap with more than just the investment piece of your financial plan:

Retirement Planning: The investments you make in retirement accounts directly affect your ability to reach long-term retirement goals.

Risk Management: Diversifying your investments is a key part of risk management in your overall financial plan.

Tax Planning: When you buy and sell investments, there are tax consequences, and the types of investments you choose can raise or lower your tax bill.

Cash Flow: As your income changes throughout life, it affects how much you can invest and how much risk makes sense for you.

Why should your Financial Planner collaborate with your Investment Advisor?

Close collaboration helps you:

Seamlessly plan and execute your investment strategy.

Adjust your financial plan as your investments and income fluctuate.

Prevent surprises when you file your taxes.

Fine-tune your retirement plan based on your investment returns

It’s especially important in Westchester County, NY where a lot of our clients have more disposable income and a higher net worth than other areas of the country. The more money you have, the more you stand to lose if something goes wrong.

Where should you start?

For most people, it makes sense to start with a Financial Planner so that you can completely understand your finances and how much you can invest. After you have enough to start investing, an Investment Advisor can help you figure out how to make your money work for you. And remember, you don’t need a lot of money to start investing. Start with what you can afford.

When the time is right, choose a Financial Planner and an Investment Advisor that have the right credentials and expertise so that you’re more likely to grow your wealth.

If you need help with your financial plan, want advice about your investments, or both, start a no-pressure conversation with an advisor. We’ll help you decide what types of professionals to work with and figure out if we’re the right fit to help you.