If you’ve been researching financial advisors or financial planners, you’re likely wondering how fees are structured.

Two common compensation models usually come up during that process: fee-only and fee-based.

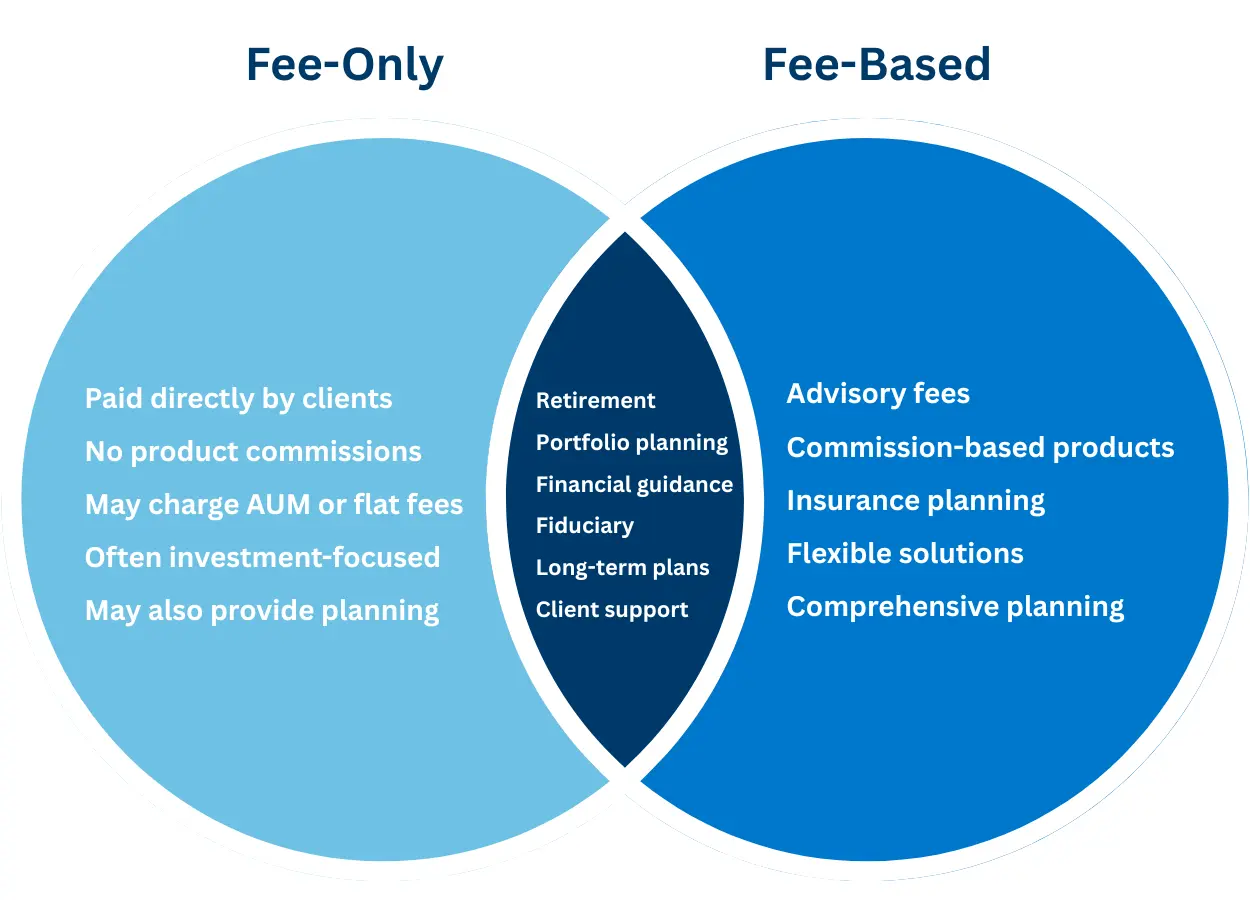

At a high level, fee-only advisors are compensated directly by clients and do not receive commissions for financial products. Fee-based advisors may charge advisory fees while also receiving commissions depending on the products or strategies being implemented.

The distinction is relatively straightforward on paper. Understanding how those models affect the planning experience, services offered, and advisor relationship is where things become more nuanced.

What Is a Fee-Only Financial Advisor?

A fee-only financial advisor is compensated directly by clients rather than through commissions tied to financial products.

Common fee-only compensation structures may include one or more of the following:

- A percentage of assets under management (AUM)

- A flat planning fee

- An hourly fee

- A one-time financial planning engagement

Fee-only firms may offer:

- Investment management

- Retirement planning

- Financial planning

- Portfolio management

- Ongoing advisory services

Some fee-only advisors provide highly comprehensive planning. Others focus primarily on investments and portfolio management.

What Is a Fee-Based Financial Advisor?

A fee-based financial advisor may receive compensation through a combination of advisory fees and commissions, depending on the products or strategies being implemented.

For example, a fee-based advisor may charge a planning or investment management fee while also recommending insurance or financial products that involve commissions.

Fee-based firms often provide services such as:

- Retirement planning

- Investment management

- Insurance planning

- Cash flow management

- Estate planning

- Business planning strategies

- Risk management analysis

Because commissions may be involved in certain situations, transparency is important. Clients should understand:

- How the advisor is compensated

- When commissions apply

- Whether the advisor acts as a fiduciary

- How recommendations are evaluated

A fee-based structure can offer flexibility for individuals or families looking for broader financial planning services beyond investment management alone.

Key Differences Between Fee-Only and Fee-Based Advisors

Although both models involve professional financial guidance, there are several distinctions worth understanding before choosing an advisor or wealth manager.

Compensation Structure

Fee-only advisors are compensated directly by clients.

Fee-based advisors may combine advisory fees with commissions, depending on the recommendations or products being implemented.

Scope of Services

Both fee-only and fee-based advisors can offer comprehensive financial planning or investment-focused services.

Planning approaches can vary significantly from one firm to another.

Some professionals primarily focus on portfolio management. Others provide broader planning that incorporates taxes, insurance, retirement income planning, estate planning, business planning, and a long-term cash flow strategy.

Implementation Flexibility

Fee-based firms may have access to certain insurance or planning solutions that involve commissions as part of implementation.

Fee-only firms typically avoid commissionable products entirely.

Neither structure is necessarily better in every situation. The right fit often depends on the complexity of the client’s financial life and the type of relationship they are looking for.

Questions to Ask Before Choosing an Advisor

If you are comparing financial advisors or wealth managers, fee structure is only one part of the evaluation process.

Here are a few questions worth asking during an introductory conversation:

- How are you compensated?

- When do commissions apply?

- Do you act as a fiduciary?

- What services are included in your planning process?

- How do you coordinate investments with taxes and retirement planning?

- How often is the plan reviewed?

- Who will I be working with long-term?

Quality financial planning often involves more than investment management alone. Communication, coordination, and long-term planning can all play an important role in the overall relationship.

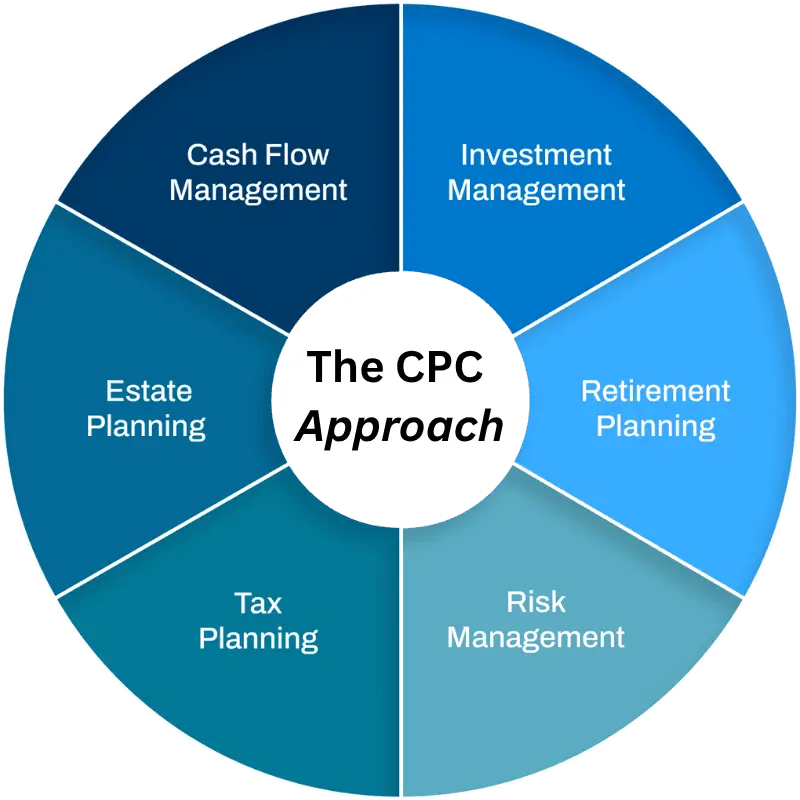

How CPC Wealth Management Approaches Planning

At CPC Wealth Management, we operate as a fee-based wealth management and financial planning firm.

Our approach is centered around comprehensive planning, with investments serving as one component of the strategy.

Many financial decisions are connected. Retirement planning can affect taxes. Insurance decisions can affect estate planning. Business ownership can influence investment strategy, cash flow planning, and long-term retirement goals.

Because of that, we focus on helping clients evaluate how those moving pieces work together.

Our planning process may include:

- Retirement planning

- Investment management

- Insurance and risk management review

- Tax-aware planning strategies

- Estate planning coordination

- Business planning considerations

- Cash flow and distribution planning

Transparency is an important part of the process. Clients should understand how recommendations are made, how compensation works, and how different strategies fit together into the financial plan.

Every individual and family has different priorities. The goal is to build a coordinated strategy designed around those priorities over time.

Which Fee Structure is Right For Me?

Understanding the difference between fee-only and fee-based financial advisors is an important step when evaluating your options.

Compensation structures can influence how an advisor relationship is structured and how recommendations are delivered. At the same time, fees alone do not fully define the quality or depth of financial planning being offered.

The better approach is to understand:

- How an advisor is compensated

- How they approach planning holistically

- The overall value the advisor provides while guiding you toward achieving your financial goals

For many individuals and families, the ideal relationship comes down to communication, transparency, and having a financial strategy that connects all the moving parts together.

If you would like to learn more about our approach, contact CPC Wealth Management to speak with an advisor.